Structural Breaks as Investment Signals: BFAST vs. CUSUM in Quito’s Stock Market During COVID-19 Pandemic

Keywords:

BFAST, CUSUM, Time Series Analysis, COVID-19, Structural Break, Stock MarketsAbstract

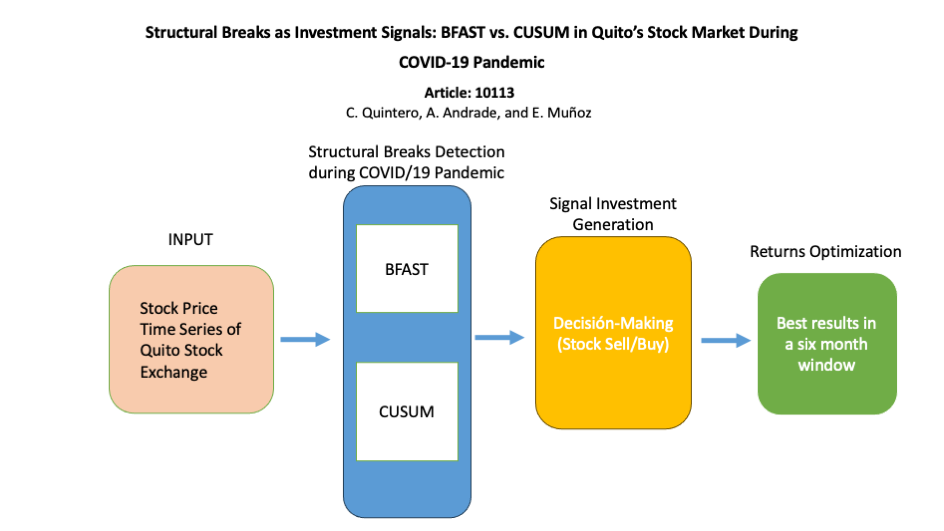

This study investigates the potential of structural

break detection in stock price time series as a tool for investment

decision-making in emerging markets. Operating under the

hypothesis that structural breaks reflect shifts in underlying

price trends, we conduct an empirical analysis of investment

performance in the Quito Stock Exchange (QSE) using monthly

average prices from 2013 to 2022 for the ten most actively

traded companies, selected for their transaction volume and

sectoral representativeness. Importantly, this period coincided

with the COVID-19 pandemic, providing a natural context to

explore how structural breaks behave under heightened market

volatility. Two algorithms—CUSUM and BFAST—are applied

and compared in terms of their ability to identify actionable

breakpoints and generate profitable buy/sell signals. Results show

that BFAST, originally developed for remote sensing applications,

consistently outperforms CUSUM: it detects a higher proportion

of successful signals, yields stronger average returns over a

six-month evaluation window (+17% in the financial sector and

+18.75% in the productive/commercial sector), and achieves

superior risk-adjusted performance as measured by Sharpe

ratios. Statistical validation using the Wilcoxon signed-rank test

confirms the significance of BFAST’s advantage (p = 0.004).

Taken together, these findings position BFAST as a robust

and economically relevant tool for financial time-series analysis,

extending its utility beyond traditional domains and offering in-

vestors a methodologically sound framework for decision-making

in volatile market environments.

Downloads

References

M. De los Baños and J. Roldán-Casas, “Análisis del grado

de eficiencia débil en algunos mercados financieros europeos.

Primer impacto del COVID-19,” Revista de economía mundial,

no. 59, pp. 243–269, 2021, number: 59. [Online]. Available:

https://doi.org/10.33776/rem.v0i59.5157

W. Li, F. Chien, H. Kamran, T. M. Aldeehani, M. Sadiq, V. Nguyen, and

F. Taghizadeh-Hesary, “The nexus between COVID-19 fear and stock

market volatility,” Economic research-Ekonomska istraživanja, vol. 35,

no. 1, pp. 1765–1785, 2022, number: 1 Publisher: Taylor & Francis.

[Online]. Available: https://doi.org/10.1080/1331677X.2021.1914125

H. Lee, “Exploring the initial impact of COVID-19 sentiment on

US stock market using big data,” Sustainability, vol. 12, no. 16,

p. 6648, 2020, number: 16 Publisher: MDPI. [Online]. Available:

https://doi.org/10.3390/su12166648

R. J. Mendoza-Rivera, J. A. Lozano-Díez, and F. Venegas-

Martínez, “Impacto de la pandemia Covid-19 en variables financieras

relevantes en las principales economías de Latinoamérica,” Economía:

teoría y práctica, no. SPE5, pp. 125–144, 2020, number:

SPE5 Publisher: Universidad Autónoma Metropolitana, a través

de la Unidad Iztapalapa, la Unidad Azcapotzalco y la Unidad

Xochimilco, División de Ciencias Sociales. [Online]. Available:

https://doi.org/10.24275/etypuam/ne/e052020/mendoza

M. L. Alzúa and P. Gosis, “Impacto Social y Económico de la COVID-

y Opciones de Políticas en Argentina,” PNUD América Latina y el

Caribe, vol. 6, pp. 1–27, 2020.

J. R. Huamán, “Impacto económico y social de la COVID-19 en el Perú,”

Revista de Ciencia e Investigación en Defensa-CAEN, vol. 2, no. 1, pp.

–42, 2021, number: 1.

K. Ceballos-Palma, K. Bermeo-Pazmiño, and L. Vásconez-Acuña,

“Covid-19 y su impacto contable en las PYMES del cantón Cuenca,”

Revista Arbitrada Interdisciplinaria Koinonía, vol. 5, no. 4, pp.

–298, 2020, number: 4 Publisher: Fundación Koinonía. [Online].

Available: https://doi.org/10.35381/r.k.v5i4.958

N. Huilcapi, K. Troya, and W. Ocampo, “Impacto del COVID-19

en la planeación estratégica de las pymes ecuatorianas,” Recimundo,

vol. 4, no. 3, pp. 76–85, 2020, number: 3. [Online]. Available:

https://doi.org/10.26820/recimundo/4.(3).julio.2020.76-85

D. Jumbo, J. Campuzano, F. Vega, and Luna, “Crisis económicas y

covid-19 en ecuador: impacto en las exportaciones,” 2020. [Online].

Available: http://scielo.sld.cu/pdf/rus/v12n6/2218-3620-rus-12-06-103.

J. Cadena, H. Pinargote, and K. Solorzano, “Mercado de valores y

su contribución al crecimiento de la economía ecuatoriana,” Revista

Venezolana de Gerencia, vol. 23, pp. 562–574, 2018. [Online].

Available: https://biblat.unam.mx/hevila/Revistavenezolanadegerencia/

/vol23/no83/4.pdf

S. K. Maya Chávez, “Impacto financiero del covid19 en empresas

que cotizan en la bolsa de valores,” Ph.D. dissertation, Politécnica

Salesiana Ecuador, Guayaquil, 2022. [Online]. Available: http:

//dspace.ups.edu.ec/handle/123456789/22307

B. EC, “Bolsa de valores de quito reporte diario 30-dic-2019,” BCE,

Quito, Tech. Rep., 2019. [Online]. Available: https://www.bce.fin.ec/

index.php/component/k2/item/281-bolsa-de-valores-de-quito

E. Muñoz, A. Zozaya, and E. Lindquist, “Satellite remote sensing

of forest degradation using NDFI and the BFAST algorithm,”

IEEE Latin America Transactions, vol. 18, no. 07, pp. 1288–

, 2020, number: 07 Publisher: IEEE. [Online]. Available:

https://doi.org/10.1109/TLA.2020.9099771

P. Verma, A. Dumka, A. Bhardwaj, A. Ashok, M. C. Kestwal, and

P. Kumar, “A Statistical Analysis of Impact of COVID19 on the

Global Economy and Stock Index Returns,” SN Computer Science,

vol. 2, no. 1, p. 27, Jan. 2021, number: 1. [Online]. Available:

https://doi.org/10.1007/s42979-020-00410-w

D. Rapach, J. Strauss, and M. Wohar, “Chapter 10 Forecasting

Stock Return Volatility in the Presence of Structural Breaks,”

vol. 3. Elsevier, 2008, pp. 381–416, book Title: Frontiers of

Economics and Globalization. [Online]. Available: https://doi.org/10.

/S1574-8715(07)00210-2

D. E. Rapach and J. K. Strauss, “Structural breaks and GARCH

models of exchange rate volatility,” Journal of Applied Econometrics,

vol. 23, no. 1, pp. 65–90, Jan. 2008, number: 1. [Online]. Available:

https://doi.org/10.1002/jae.976

V. Chatzikonstanti, “Breaks and outliers when modelling the volatility

of the U.S. stock market,” Applied Economics, vol. 49, no. 46,

pp. 4704–4717, Oct. 2017, number: 46. [Online]. Available: https:

//doi.org/10.1080/00036846.2017.1293785

K.-L. Xu, “Powerful tests for structural changes in volatility,” Journal

of Econometrics, vol. 173, no. 1, pp. 126–142, Mar. 2013, number: 1.

[Online]. Available: https://doi.org/10.1016/j.jeconom.2012.11.001

R. L. Brown, J. Durbin, and J. M. Evans, “Techniques for

Testing the Constancy of Regression Relationships Over Time,”

Journal of the Royal Statistical Society: Series B (Methodological),

vol. 37, no. 2, pp. 149–163, 1975. [Online]. Available: https:

//doi.org/10.1111/j.2517-6161.1975.tb01532.x

D. W. K. Andrews, “Tests for Parameter Instability and Structural

Change With Unknown Change Point,” Econometrica, vol. 61, no. 4,

pp. 821–856, 1993, number: 4 Publisher: [Wiley, Econometric Society].

[Online]. Available: https://doi.org/10.2307/2951764

D. W. K. Andrews and W. Ploberger, “Optimal Tests when a Nuisance

Parameter is Present Only Under the Alternative,” Econometrica, vol. 62,

no. 6, pp. 1383–1414, 1994, number: 6 Publisher: [Wiley, Econometric

Society]. [Online]. Available: https://doi.org/10.2307/2951753

C.-M. Kuan and K. Hornik, “The generalized fluctuation test: A

unifying view,” Econometric Reviews, vol. 14, no. 2, pp. 135–161, Jan.

[Online]. Available: https://doi.org/10.1080/07474939508800311

P. Sánchez, “Cambios estructurales en series de tiempo: una

revisión del estado del arte,” pp. 115–140, Apr. 2008. [Online].

Available: http://www.scielo.org.co/scielo.php?script=sci_arttext&pid=

S1692-33242008000100007

IEEE LATIN AMERICA TRANSACTIONS , Vol. 7, No. 7, Oct 2020

J. Bai and P. Perron, “Computation and analysis of multiple structural

change models,” Journal of Applied Econometrics, vol. 18, no. 1, pp.

–22, 2003. [Online]. Available: https://doi.org/10.1002/jae.659

A. Zeileis, C. Kleiber, W. Krämer, and K. Hornik, “Testing and dating

of structural changes in practice,” Computational Statistics & Data

Analysis, vol. 44, no. 1, pp. 109–123, Oct. 2003, number: 1. [Online].

Available: https://doi.org/10.1016/S0167-9473(03)00030-6

J. Haywood and J. Randal, “Trending seasonal data with multiple

structural breaks. NZ visitor arrivals and the minimal effects of

/11,” Mar. 2008. [Online]. Available: https://www.researchgate.net/

publication/253383381

G. V. P. Alarcón and J. C. O. Maldonado, “Impacto financiero

del COVID 19 en las instituciones de economía popular y

solidaria del Ecuador, año 2021,” Visionario Digital, vol. 6,

no. 3, pp. 97–122, Jul. 2022, number: 3. [Online]. Available:

https://doi.org/10.33262/visionariodigital.v6i3.2197

J. C. Chia-Shang, K. Hornik, and K. Chung-Ming, “MOSUM tests for

parameter constancy,” Biometrika, vol. 82, no. 3, pp. 603–617, Sep.

, number: 3. [Online]. Available: https://doi.org/10.1093/biomet/

3.603

J. Verbesselt, R. Hyndman, G. Newnham, and D. Culvenor, “Detecting

trend and seasonal changes in satellite image time series,” Remote

Sensing of Environment, vol. 114, no. 1, pp. 106–115, Jan. 2010,

number: 1. [Online]. Available: https://doi.org/10.1016/j.rse.2009.08.014

M. Schultz, J. Verbesselt, V. Avitabile, C. Souza, and M. Herold,

“Error Sources in Deforestation Detection Using BFAST Monitor on

Landsat Time Series Across Three Tropical Sites,” IEEE Journal of

Selected Topics in Applied Earth Observations and Remote Sensing,

vol. 9, no. 8, pp. 3667–3679, Aug. 2016. [Online]. Available:

https://doi.org/10.1109/JSTARS.2015.2477473

K. Grogan, D. Pflugmacher, P. Hostert, J. Verbesselt, and R. Fensholt,

“Mapping Clearances in Tropical Dry Forests Using Breakpoints,

Trend, and Seasonal Components from MODIS Time Series: Does

Forest Type Matter?” Remote Sensing, vol. 8, no. 8, pp. 1–27, Aug.

, number: 8. [Online]. Available: http://doi.org/10.3390/rs8080657

J. Reiche, S. de Bruin, D. Hoekman, J. Verbesselt, and M. Herold, “A

Bayesian Approach to Combine Landsat and ALOS PALSAR Time

Series for Near Real-Time Deforestation Detection,” Remote Sensing,

vol. 7, no. 5, pp. 4973–4996, Apr. 2015, number: 5. [Online]. Available:

http://doi.org/10.3390/rs70504973

Y. Gao, J. V. Solórzano, A. Quevedo, and J. O. Loya-Carrillo, “How

BFAST Trend and Seasonal Model Components Affect Disturbance

Detection in Tropical Dry Forest and Temperate Forest,” Remote

Sensing, vol. 13, no. 11, p. 2033, Jan. 2021, number: 11 Publisher:

Multidisciplinary Digital Publishing Institute. [Online]. Available:

https://doi.org/10.3390/rs13112033

Z. Zhu and C. E. Woodcock, “Continuous change detection and

classification of land cover using all available Landsat data,” Remote

Sensing of Environment, vol. 144, pp. 152–171, Mar. 2014. [Online].

Available: https://doi.org/10.1016/j.rse.2014.01.011

J. Verbesselt, R. Hyndman, A. Zeileis, and D. Culvenor, “Phenological

change detection while accounting for abrupt and gradual trends in

satellite image time series,” Remote Sensing of Environment, vol. 114,

no. 12, pp. 2970–2980, Dec. 2010, number: 12. [Online]. Available:

https://doi.org/10.1016/j.rse.2010.08.003

W. N. Venables and B. D. Ripley, Modern Applied Statistics with

S-PLUS. Springer Science & Business Media, Apr. 2013, google-

Books-ID: tovgBwAAQBAJ. [Online]. Available: https://doi.org/10.

/2532871

“Evaluation of polarimetry and interferometry of sentinel-1A SAR data

for land use and land cover of the Brazilian Amazon Region | Semantic

Scholar.” [Online]. Available: https://www.semanticscholar.org/paper/

Evaluation-of-polarimetry-and-interferometry-of-SAR-Diniz-Gama/

abe6bae11afac257ab220047203ee6213f0f6a2f

J. Verbesselt, D. Masili¯unas, A. Zeileis, R. Hyndman, M. Appel,

M. Jung, A. Mîrt,, P. N. Bernardino, and D. Kong, “bfast: Breaks

for Additive Season and Trend,” Oct. 2024. [Online]. Available: